It is a section from 0xresearch newsletter. To read full versions, subscribe.

recently Report Ludge evaluate blockchain based on GDP by investment:

“… It is more appropriate to compare decentralized blockchain for sovereign nations and their economies rather than web 2 companies or products due to embedded currency.”

Here is the GDP formula: C + i + G + (XM)

C is consumed, I have business investment, g government expenditure, x export and M is import, so XM is pure export.

Fidelity uses Eth as an example. Therefore, when you transfer the GDP formula on the Etharium Blockchain Matrix:

- C = what users are spending as gas, uniswap or mint to use an NFT.

- I = quantity of stacked assets or capital in liquidity pool.

- G = Ethereum Foundation Expenditure, issued ETH to verifications.

- XM = How much stabelcoin mint/burnt, the bridge flows from other chains and dipin rewards.

You can see the entire table here:

This is a broad effort by Fidelity, but it provokes some questions.

GDP is a measure of domestic production. Think “value of everything made here.” When a country exports, it is domestic production. When it imports, it costs. So we import “net” for GDP.

But if millions of stabelins are closed at (import) or (export) atherium, a blockchain’s “GDP” blots, even if nothing is productive.

Conversely that when a stabelcoin is onchain, or when a helium minein is paid in tokens to provide a useful mobile cellular service. These are producers “imports” that will count correctly towards the “GDP” of a blockchain.

Therefore measuring “net exports” by Bridge Flow is an ideological sound, but it should be responsible for CEX cold-wallet sweeps, as is suitable by Dan Smith of Blockworks.

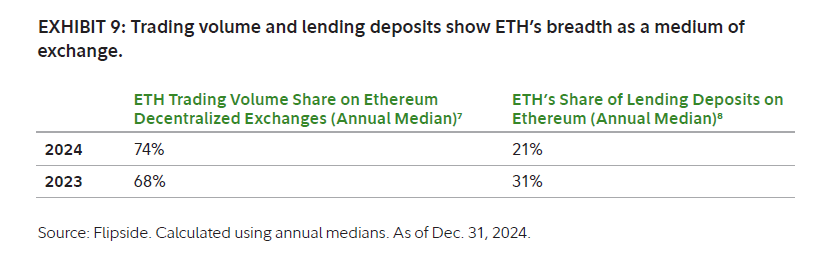

In the valuation model of Fidelity, it is also clear that L1 tokens should be given importance on a medium basis of the exchange and store of value: “money”, or more especially: a medium.

Fidelity argues: “Ether is a major trading pair on exchanges and serves as a primary asset to borrow against it.”

I think the “medium of exchange” aspect of money looks best, but is silent on the “unit of account” aspect.

Initial crypto investors have questioned the ability of L1 tokens to act as a unit of account. As John Fafar wrote Back in 2017:

“It is very simple to believe that people will use the rough to pay, which they use to pay to pay, which is necessary to replace their value reserves through the payment rail at the time of payment, which is required to pay the time of payment in the required exact amount and for as much time as possible.”

The account abstract (ERC-4337) even a formal form to this reality, as it enables to pay a gas fee in any ERC-20 token. This significantly improves the user experience, but it removes the need to deposit ETH, which reduces the “monetary premium” of the L1 tokens.

I think the last aspect of GDP analogy is somewhat stressed for stacked Ath under the “Investment” bucket of GDP.

Stacking shuts down existing assets, but no new productive capacity is created.

In the economist jargon, it does not push the “limit of production possibilities” like investment in the real economy.

So in blockchain GDP “I” loses its future link for future development.

Worse than this: LP can migrate and earn a purely extractive aircraft or MEV.

Get news in your inbox. Explore blockwork newsletters: