This is a segment from the forward guidance newsletter. To read full versions, subscribe.

We are all navigating crosscrackers of the next stage of tariff war, dollar positioning and rates.

Signed and passed with “Big Beautiful Bill”, the Trump administration’s gaze is now coming back to the tariff.

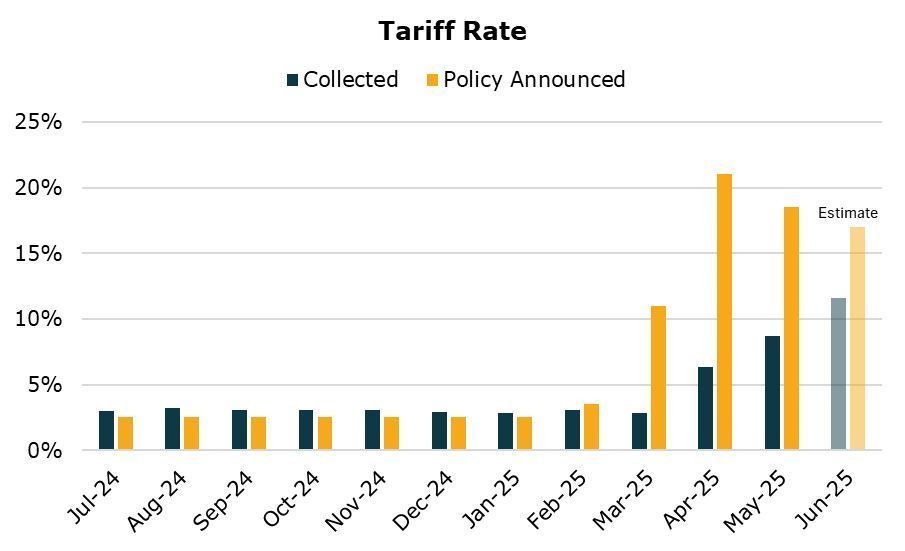

True tariff rates are changing these days, and the exact number continues to fluctuate.

Said that, based on the actual goods container volume transactions, we can approximate the current effective tariff rate of 21% on US imports – below 54% at the peak of liberation day.

It causes delayed effects for collection of these duties over the dynamic range. Such bounce in the collection takes time to fully ramps and operate, and therefore the actual tariffs collected are about half of the right rates right now.

It is clear that some form of tariff strategy is in place. But assuming that they would go back to the elective rate of 5%, it is unrealistic.

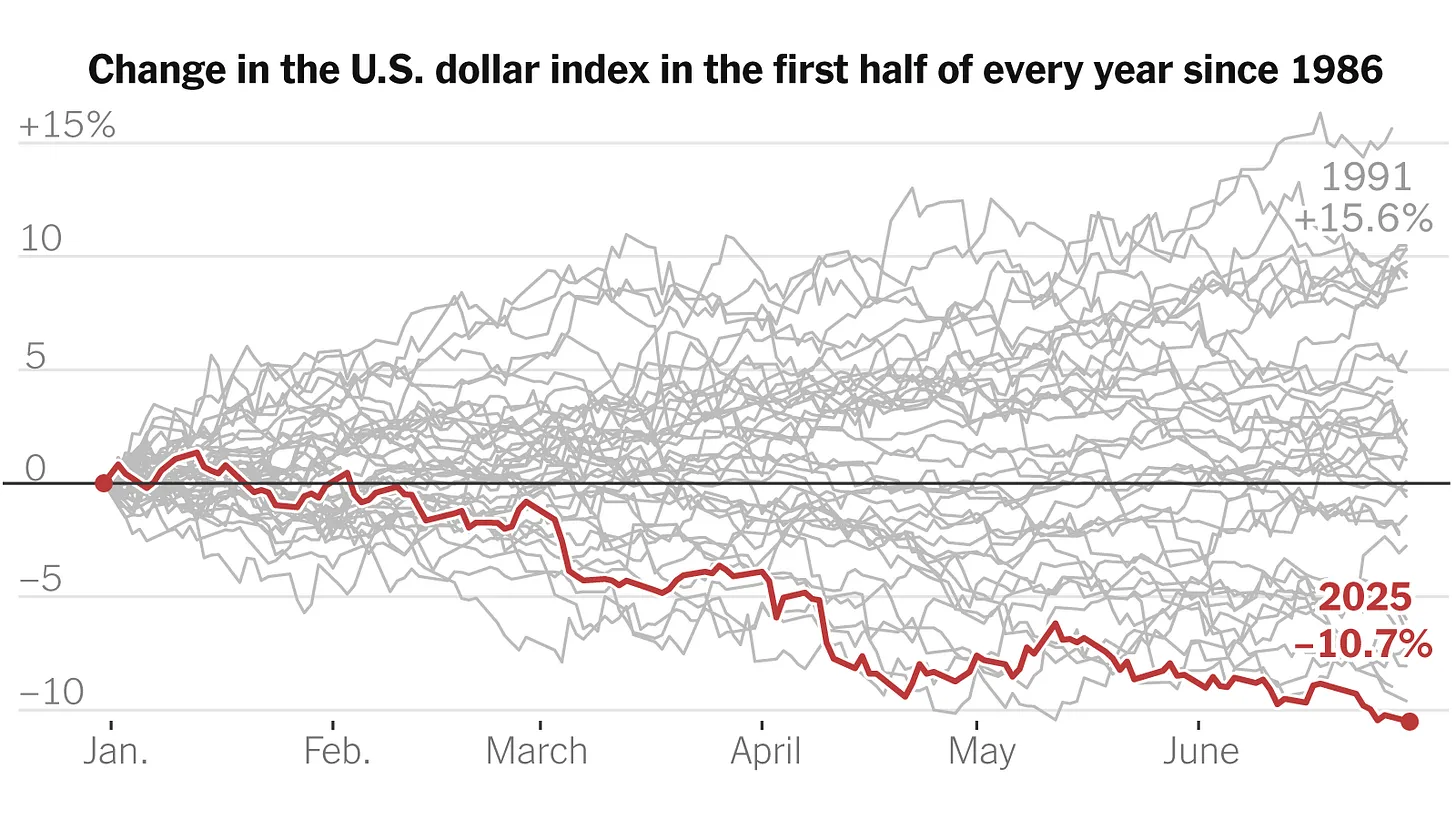

Keeping all this together, it is time to think about how this crosscrett locates itself along the path of currencies and monetary policy. As we can see below, the dollar is now below 10.7% year, which is one of the biggest drawdowns for the first half of the year.

Mechanically, it makes sense to be the primary exhaust valve for the effect of tariffs for the dollar as it collects the interest rate difference and the path of monetary policy. They are inspired by the expectations of inflation, as well as cross -border capital flow.

The widespread consensus is that this dynamics will continue to reduce the dollar meaningfully and once turbocharged, it becomes clear who will convert Geom Powell as the chairman of the Federal Reserve.

If a person on the new chair is committed to the 300-base point cut, then avoiding Trump-and if the person can convince the committee to follow them-then the dollar is lucky for more weakness.

This structure makes all fundamental understanding. The issue: This is currently a view of consensus in the markets, as we go to summer doldrums that often test the situation as instability.

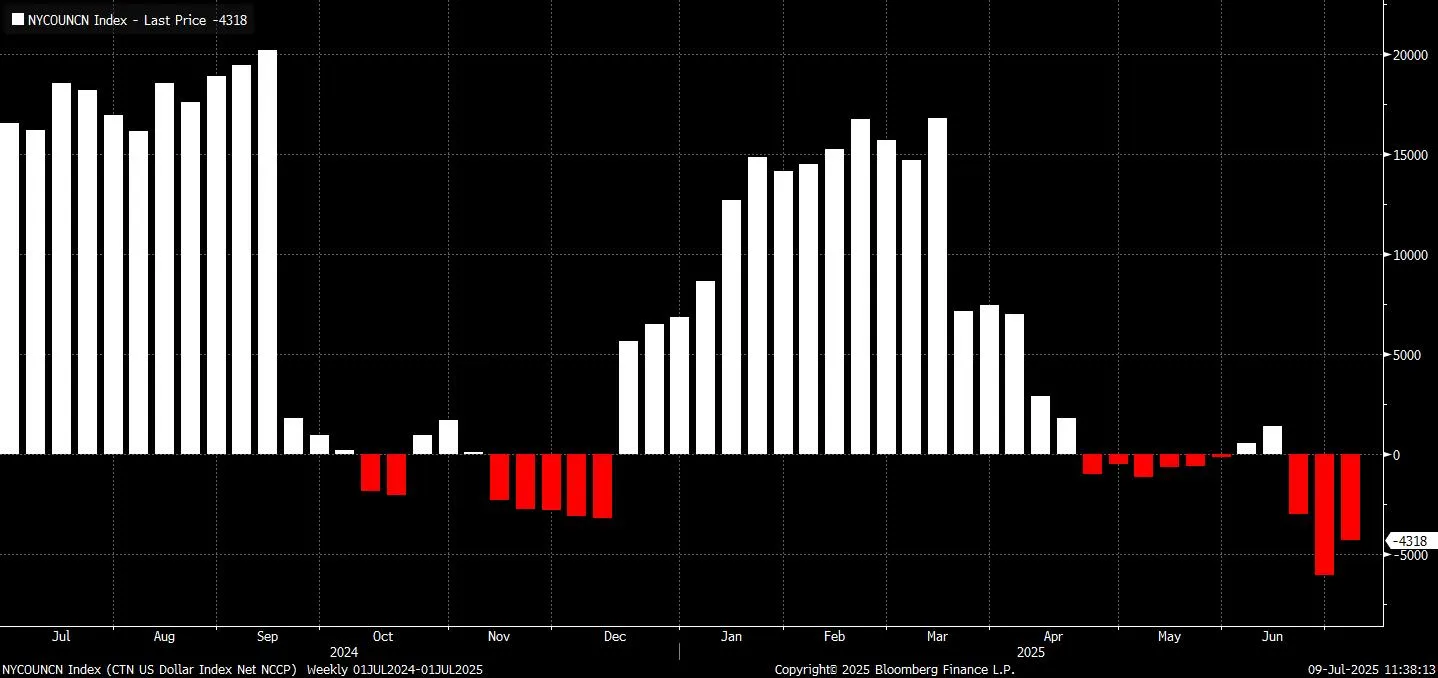

Given the current CFTC data, the dollar condition is the most recession that is in years:

Therefore, despite the basic principles, pointing to the devaluation of the meaningful dollar, I think thesis will be tested in summer, given that it is a crowded business.

Get news in your inbox. Explore blockwork newsletters: