This is a section from the breakdown newsletter. To read more versions, Subscribe,

“What does the market expect almost never happens.”

– Jamie Dimon

American equities again hit all-time high hits this week, and it is difficult to know what it means.

Consider that it is also the week that is the President of the United States called The chairman of the Federal Reserve is a “Sunnaskul”.

Worse than name-koling, the President said that FOMC should reduce interest rates by 1%, clearly the government can save “a trillion dollars per year”.

This is the definition of “fiscal dominance”: when a central bank artificially keeps the interest rates to adjust the deficit expenses, with unimaginable results to follow it.

Luckily, we are not there yet.

Chair Powell still has 10 months of job and the President has not come to know how to fire him, although he is still trying.

(We live in a bizarre timeline where Marble volume Federal Reserve Bhawan is relevant to monetary policy included in the masks.)

But the leading candidate to replace Powell, Kevin Wars, is offering to subdue the Fed in the White House in exchange for appointment – a Fastian deal for which we will pay all the price.

Something seems to be concerned about markets: Economists have long warned that fiscal dominance is guaranteed to reduce dollar, government debt and trust in the entire American economy.

But American shares are continued and treasury bonds usually seem unaffected.

Veteran hedge fund manager Stanley Druknamiller once said that the best economist he knew that the stock market was, so perhaps it means that we can rest?

Can we take the market’s Sangin price action as support for standing tariffs and fed bullying? Or is it a prediction that he will not do what he says he will do?

Alternatively, can the market accept that tariffs and monetary policy are currently very unstable to predict?

Or is it an indication that the policy does not matter as much as we thought?

I am probably uprooting it.

Fed Governor Christopher Waller, who does not promote for the replacement of Powell, said this week said that “Target’s reverse risk to limit inflation and inflation, we should not wait until we have a labor market deteriorated before cutting the policy rate.”

The rate cut in the market is very much liked, so perhaps it matters all.

Or it can happen nobody In this sense, because AI is on the verge of changing everything anyway?

This week, Mark Zuckerberg Said This meta is starting to see the initial glimpse of self-reform with “(AI) model” and that “the supervision is now in sight.”

In particular, he thinks that we can be two or three years away from artificial intelligence that are crossing human intelligence – not only in coding or newsletter writing, but in all fields.

If the world of Superintendent AIS is less than three years away with the ability of self-reform, do we care about whether Fed Fund is 1% or 5%? Or are tariffs 0% or 50%?

This would be a whole new world, possibly, and the best economist Stanley Druknamiller knows that it would be a good.

Let’s hope that this is correct.

Importing is inflating:

An academic Study This suggests that Tariff has increased the price of imports faster than the price of household goods. This has not yet affected the American economy, but Ben Castleman Tell me This does not mean that it will not happen. Morgan Stanley analyst Think that the economy should begin to show the negative effects of tariffs in the third quarter (which is now).

For now, things are very good:

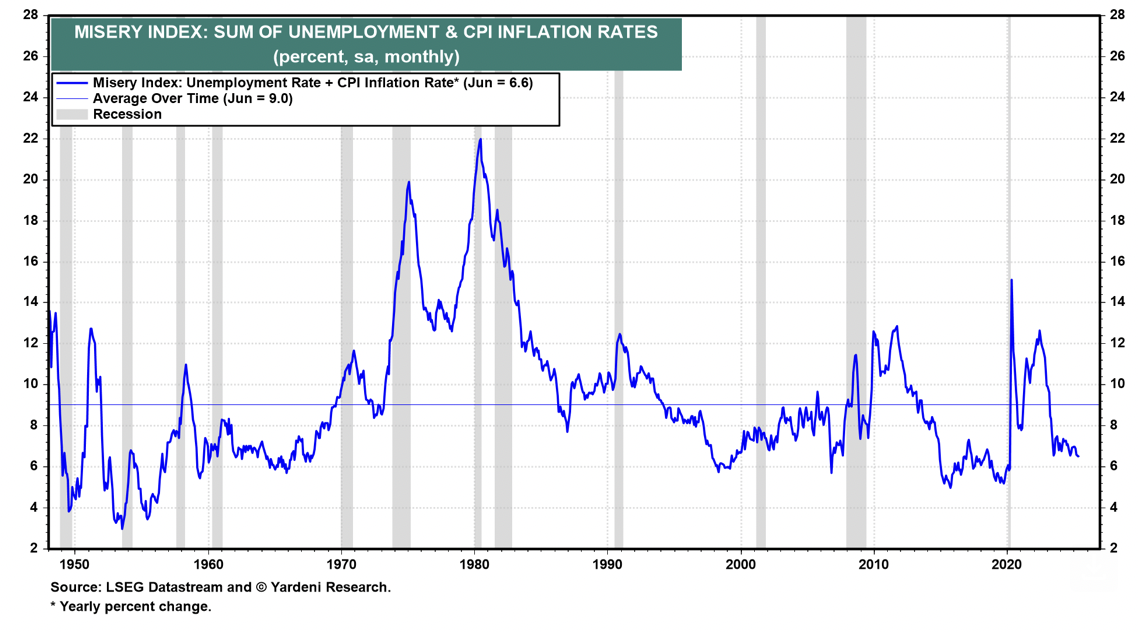

Ed Yardni stated that the “sorrow index”-the rates of inferiority and inflation are below the summer average.

Economists have recently been very worried:

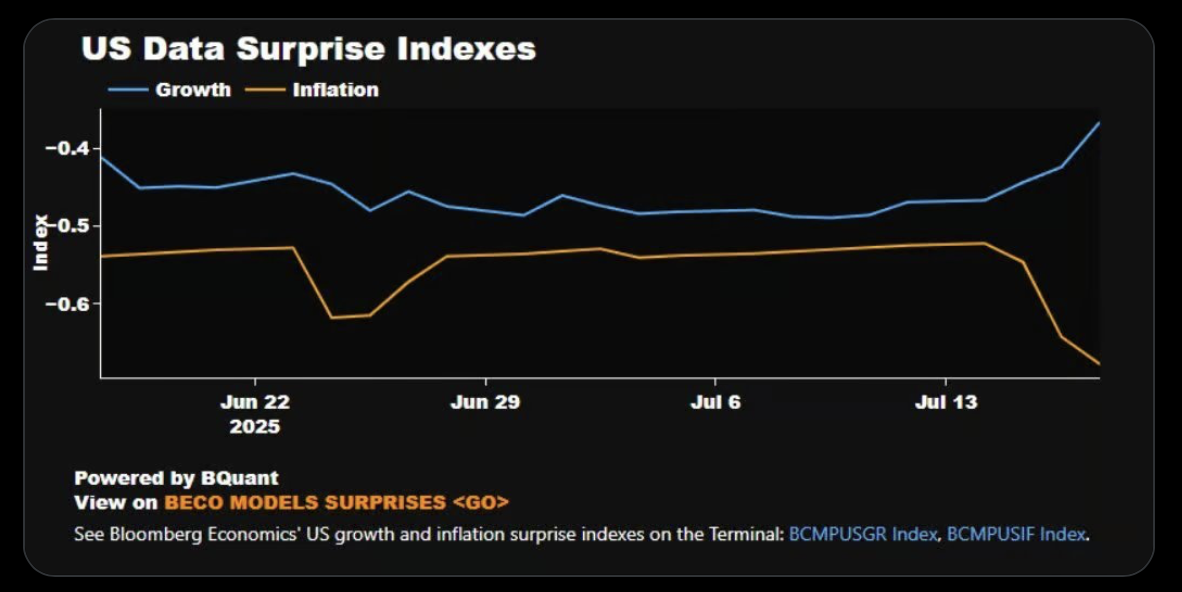

Anna Wong Note which has recently been better than the expectations of American development and inflation figures.

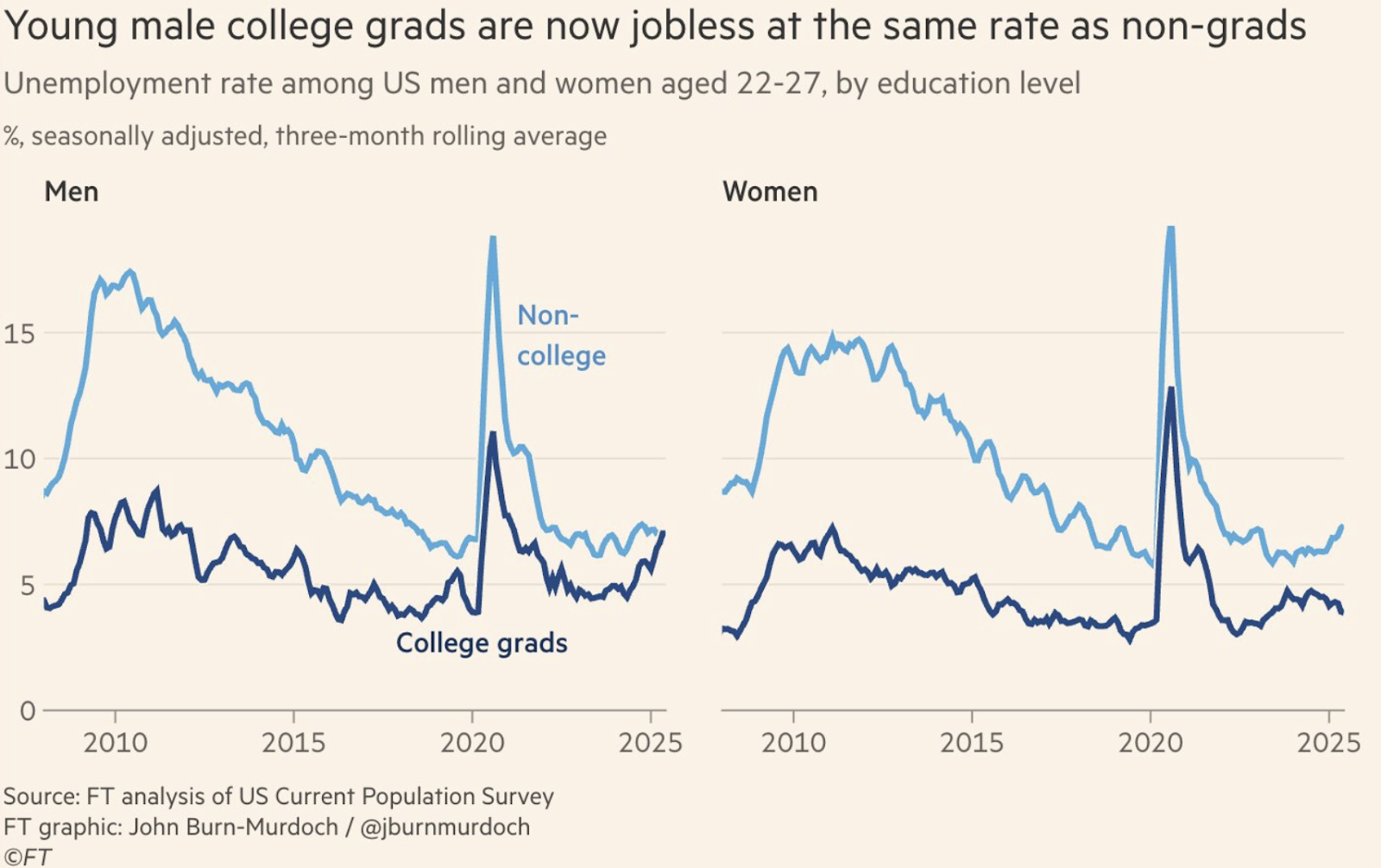

This male is worse than expected for college grade:

Ft columnist John Burn-Murdoch Note College degrees are expected to be unemployed as young men without degrees. Graduates of women college continue to fare better, perhaps because they are more likely to work in health care.

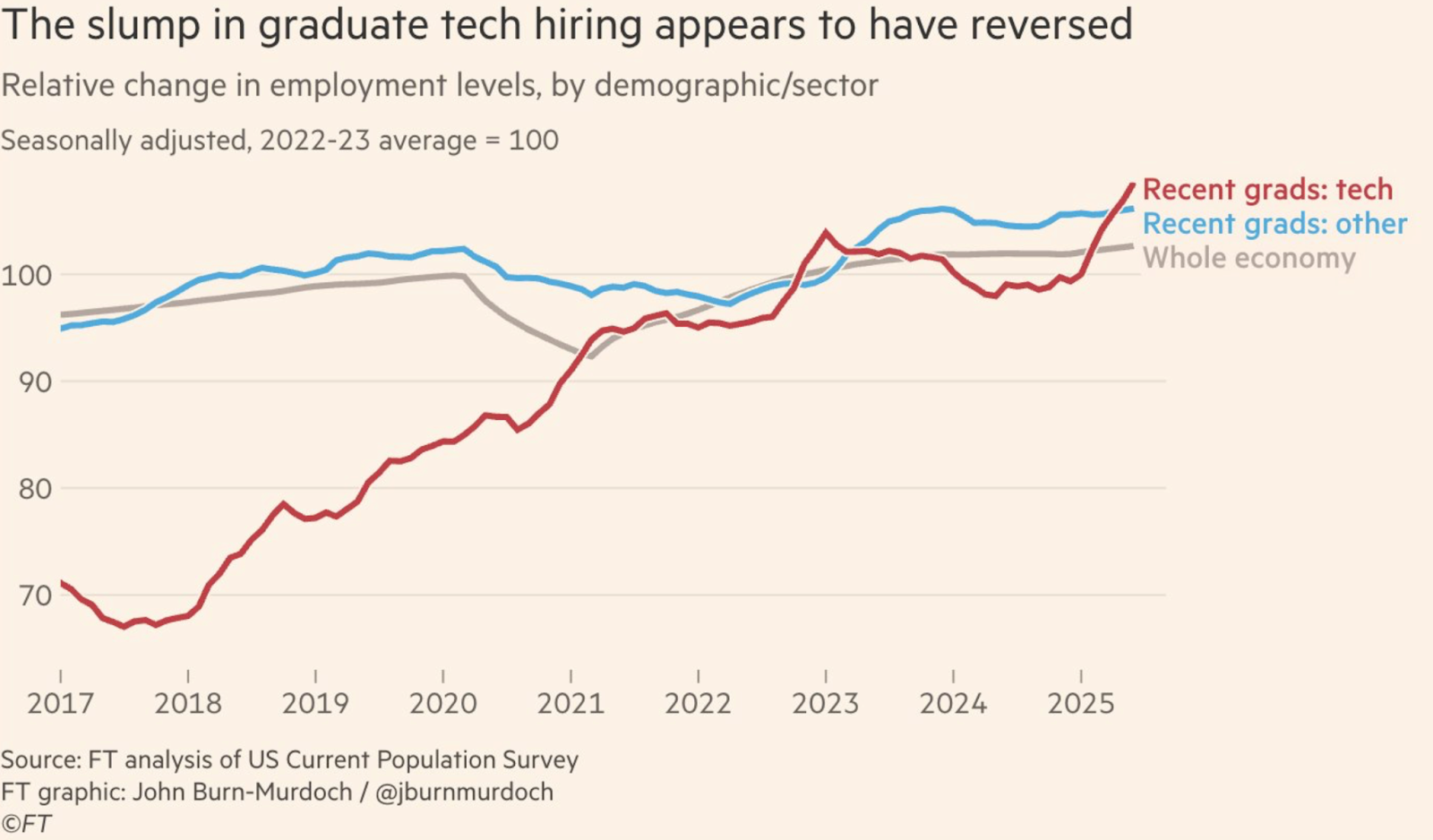

Do not blame Comp SCI:

Unlike the popular belief, along with burn-mark notes “relative to the pre-generative AI era, recent grades have secured coding jobs at the same rate, as they have got a job, if not a little more.”

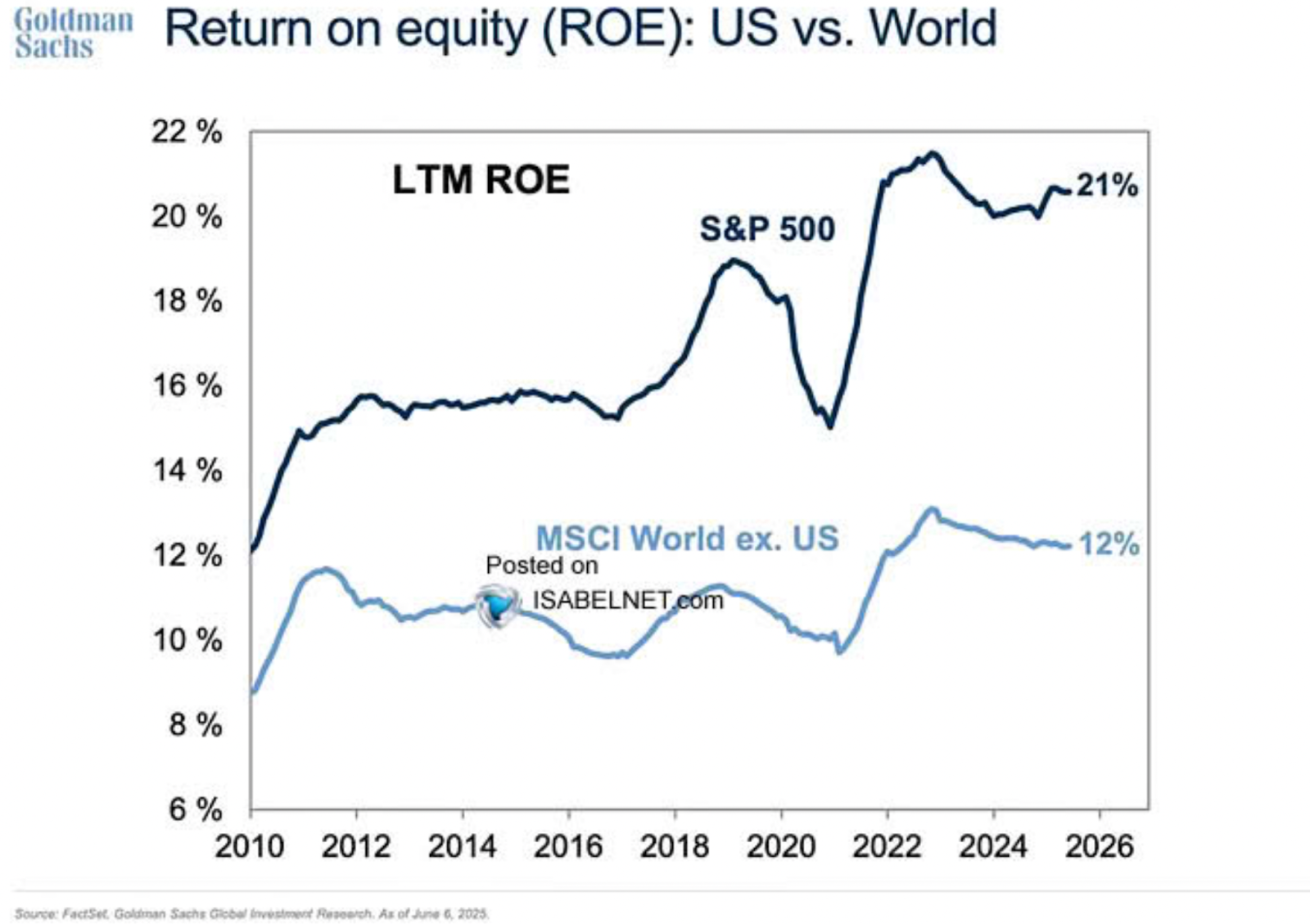

American companies are still the best:

Goldman Sachs reminds us that large American companies are far more profitable than companies in the rest of the world. They can be even more: Both Amazon and Microsoft were asked to reduce their payroll by thousands of employees this week, reportedly because they believe they could ask AI to work more than AI.

On the other hand…

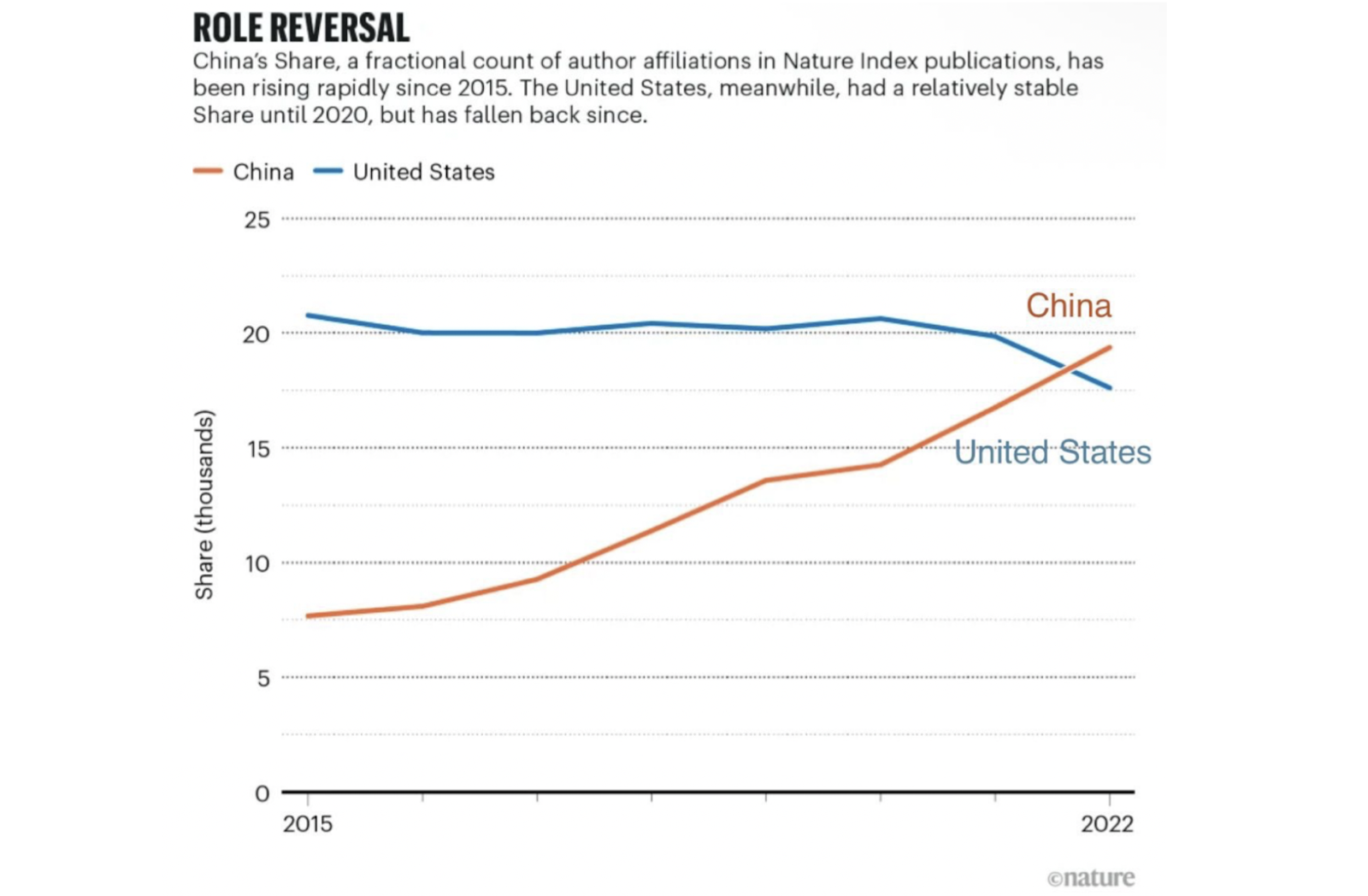

By MultipleChina has pulled forward from America in scientific research. Maybe US mega tech companies will make a difference. But if we are in the two-country race for the Superintendent, now it seems that there is a bad time for the government to cut the research grant.

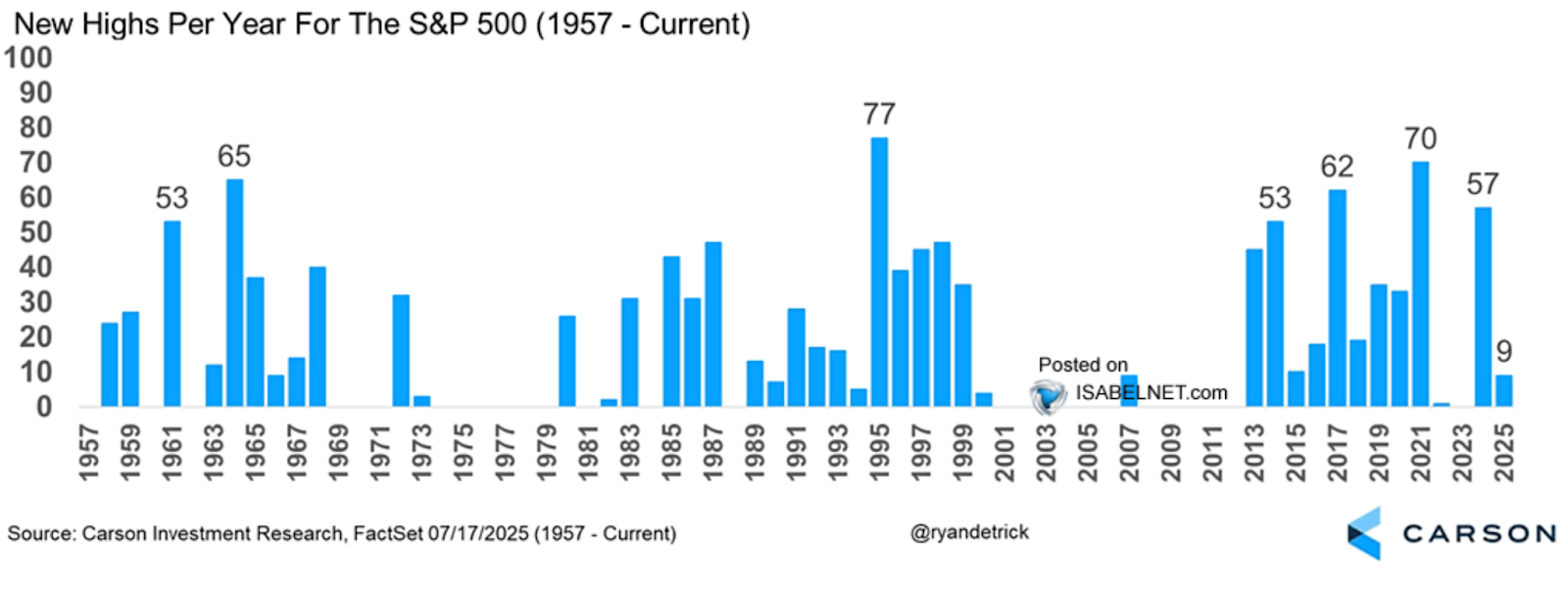

New highs are normal:

This graph of @Ryandetrick is a reminder that making new height is ideal for American equity. The total nine of this year is still very minor.

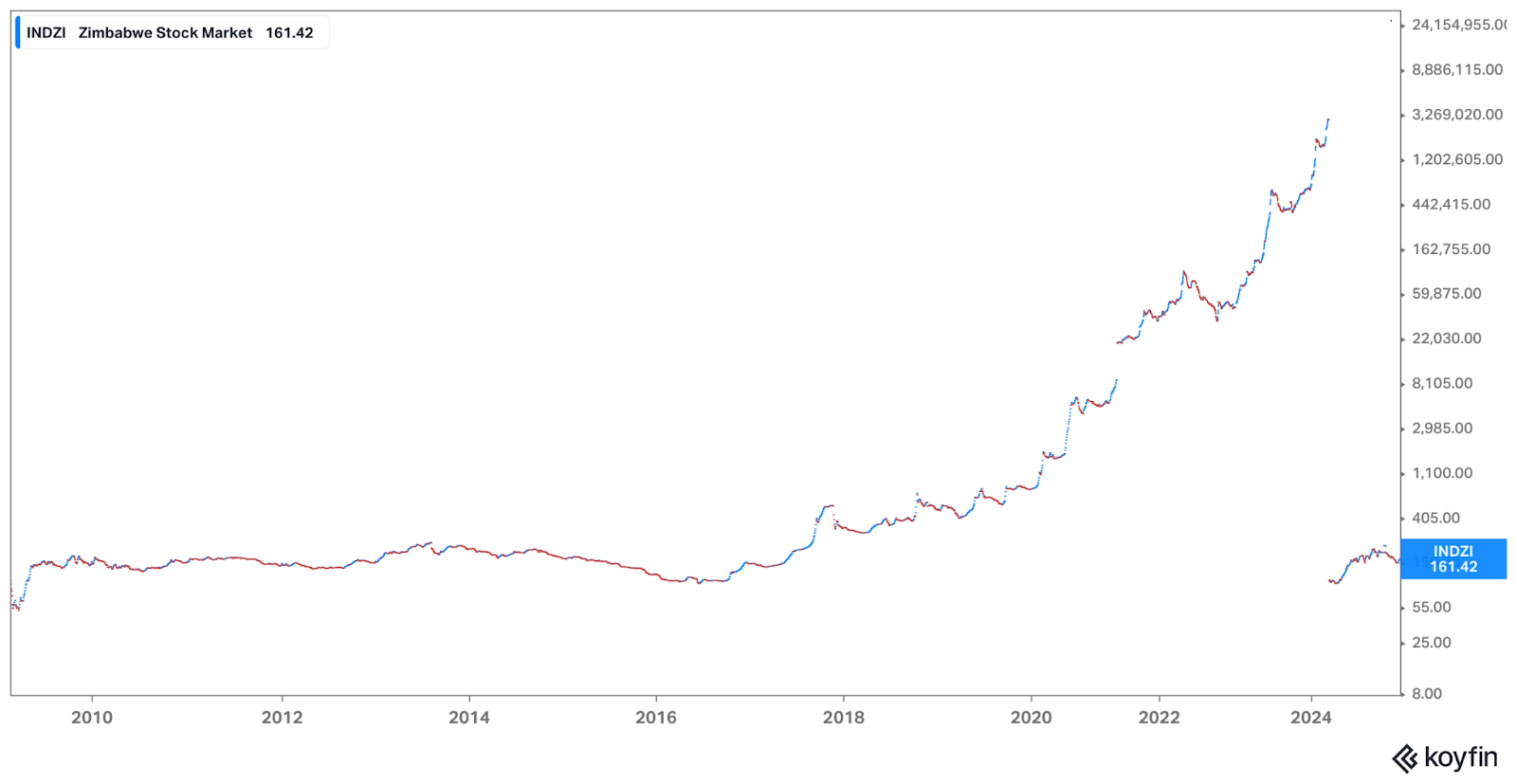

Zimbabwe stocks made a lot of new highs:

Zimbabwe’s stock prices jumped during the Hyperineflation match starting in 2019 – just because the stock is shown in a local currency. When the currency was revalved in March, the shares were also rebuilt.

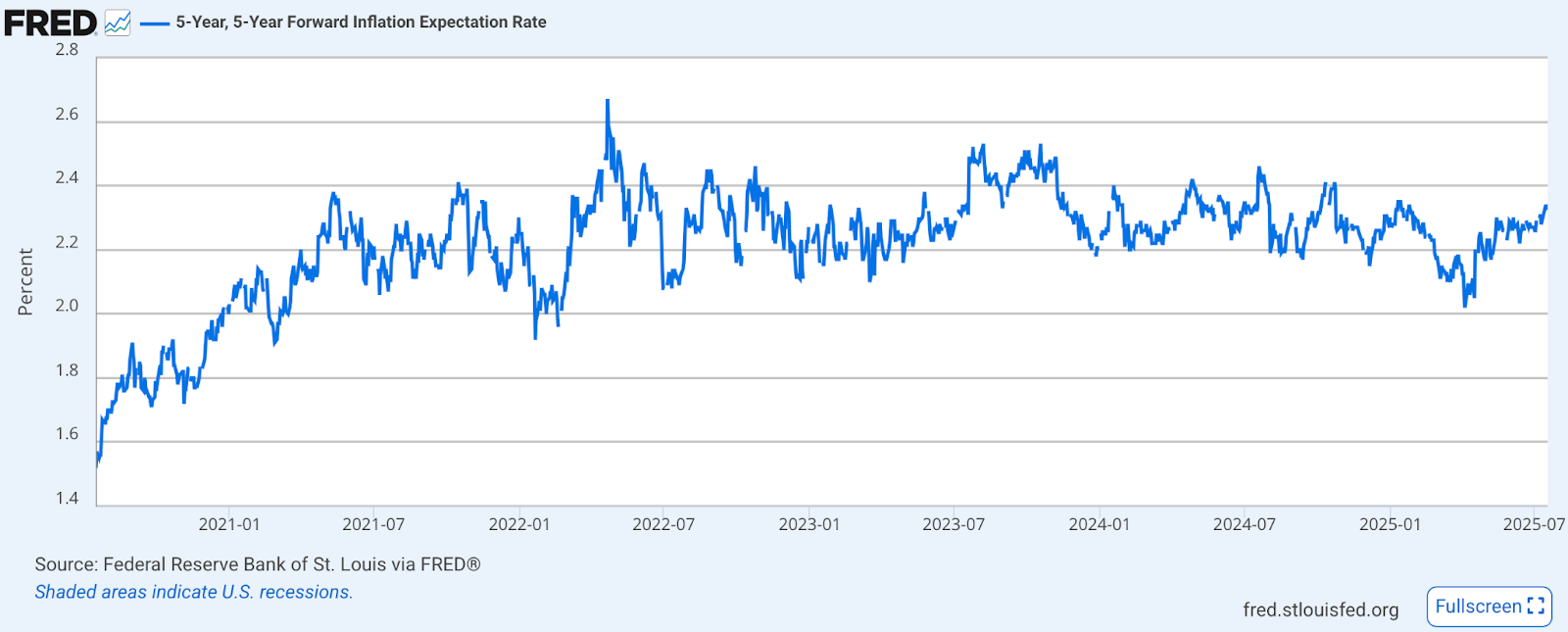

Not yet Zimbabwe:

Despite the increasing risk of fiscal dominance, the market for further inflation expectations means that American inflation will be just 2.3% in five years – which will be very good news for the world.

If the market is having faith in the fed, shouldn’t we all do it?

Jamie Dimon will tell you how it works, but let’s hope that she is wrong.

There is a great weekend, future readers.

Get news in your inbox. Explore blockwork newsletters: