This is a segment from the forward guidance newsletter. To read full versions, subscribe.

As with economic data these days, Satan is in all details.

Today we received the latest jobs report, and the topline data looked great.

- Non-pharmal payroll 100K came on the 147K vs. unanimous estimates.

- The unemployment rate fell down to 4.1%, which was up to 4.3%from the increase forecasts.

4.1% unemployment rate is stronger than their June summary of economic estimates than recent estimates of FOMC, and there is no possibility of cutting from the table on July: July:

The main vector of this topline strength in the labor market is a decreasing labor force. This is due to the demolition of immigration since Trump took over.

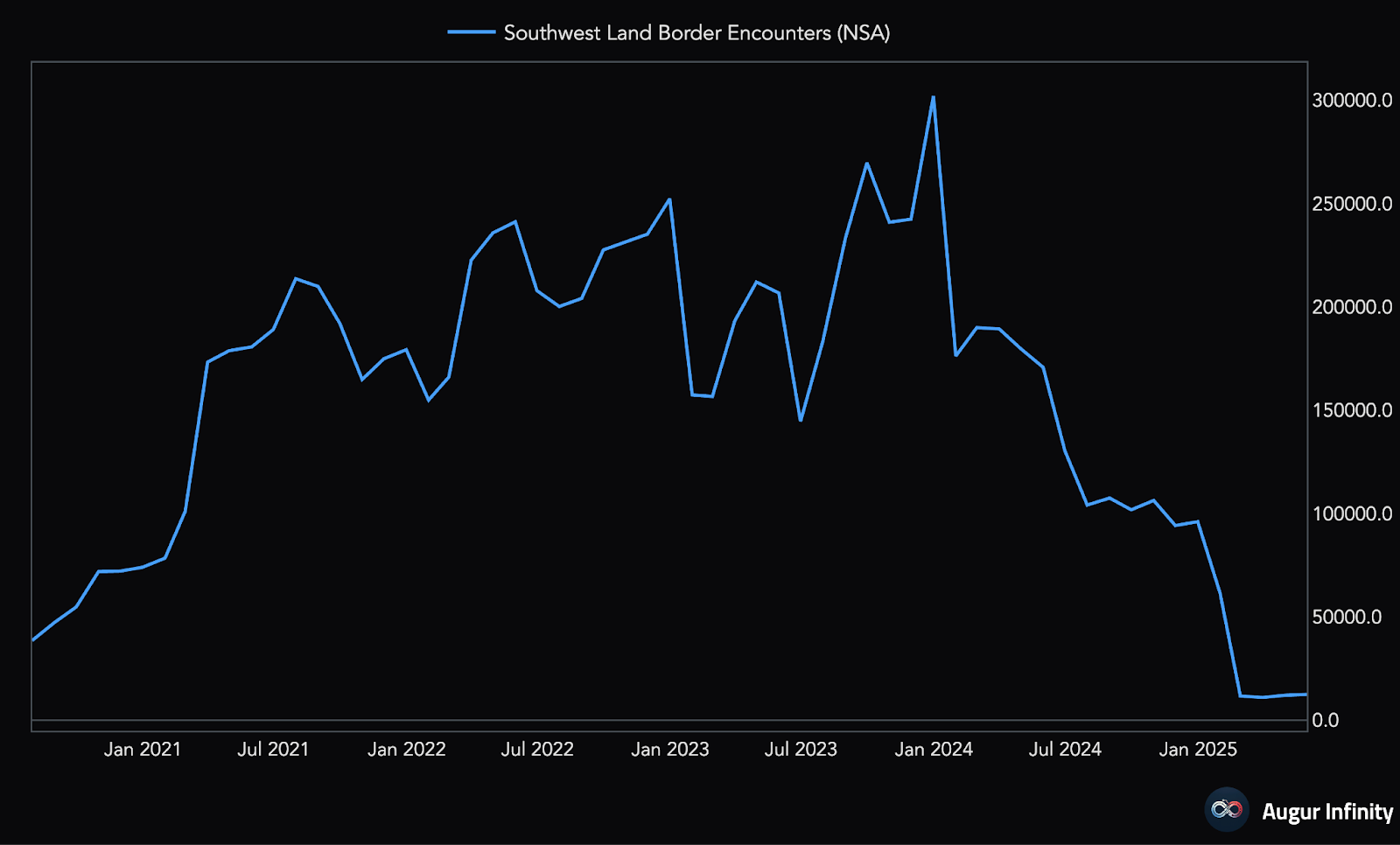

Looking at the land border crossing, we can see that these are pits.

A year ago, we saw this dynamic in reverse:

- The huge level of immigration under the Biden administration increased the labor force, which increased the mechanical unemployment rate, as it took time for those new entry to get jobs. And, in the meantime, those new entry are considered unemployed in BLS data.

- This was the same that caused the false-and-signs of the SAHM rule, due to which the fed 50bps were cut in quick order.

Keep it together: In the same way that immigration was causing the mechanical weak labor market in the last September, now we see a mechanically strong labor market.

It is dynamic shroud as to what is deepening in the data.

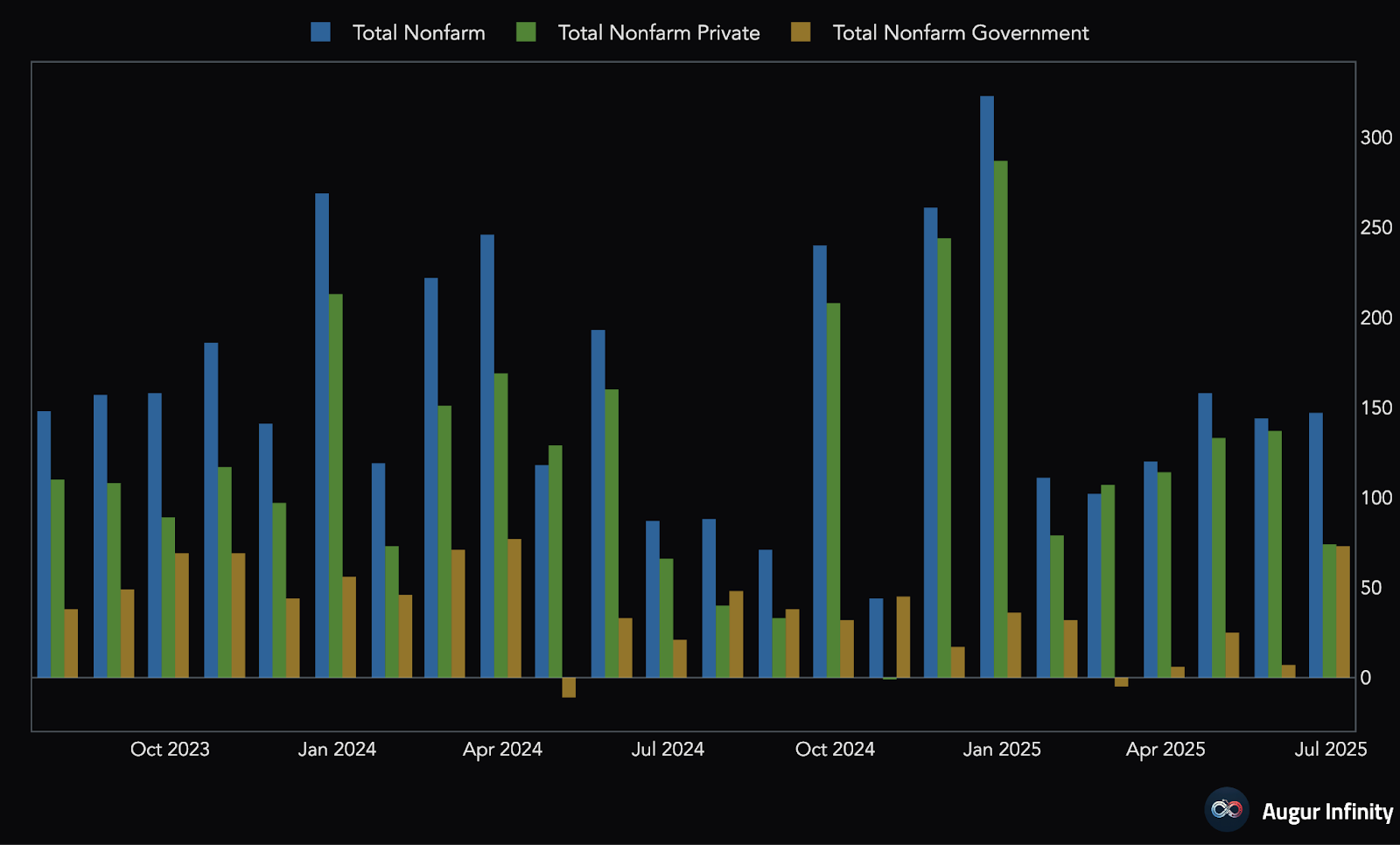

Below 105K expectations, private payroll came to 74k. The reason for the important reverse surprise came from government payroll, which increased from 7K to 73K last month:

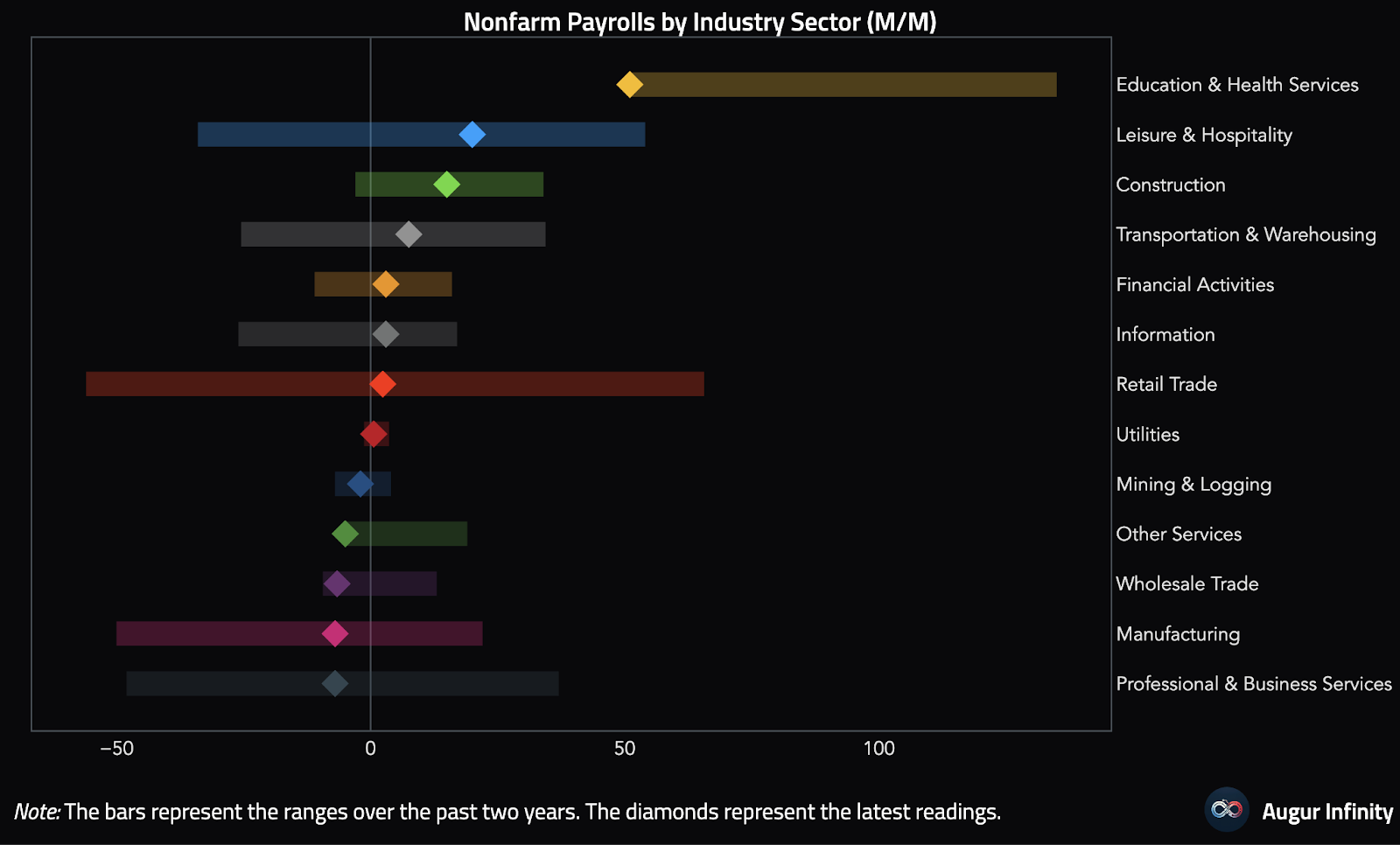

Given the industries that have reduced payroll growth, education and health services, it is minimal, which is notable, as they have been the primary driver of payroll growth in recent years.

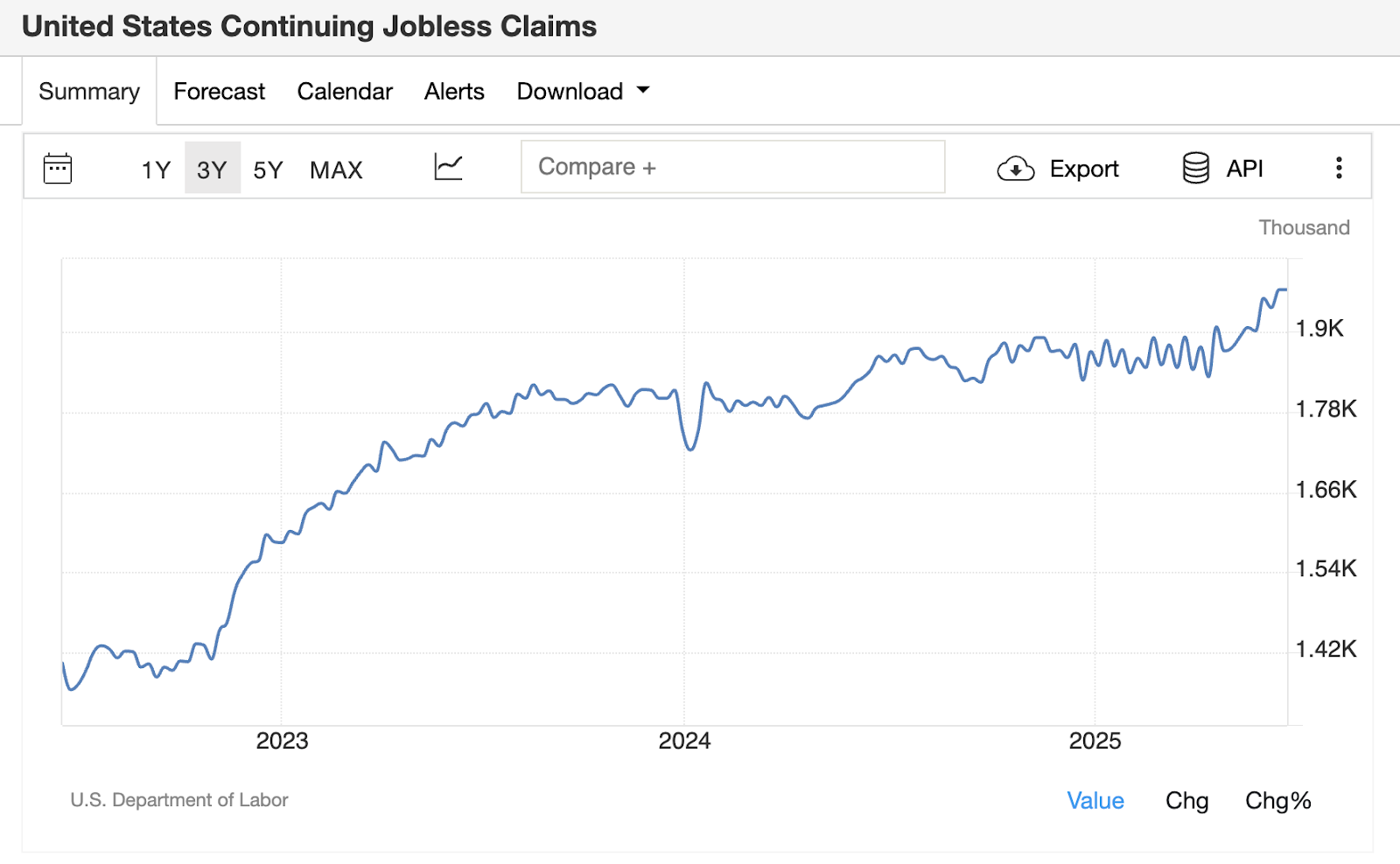

This delicate balance in the labor market is mostly felt by those who are currently unemployed and are extremely difficult to get a new job.

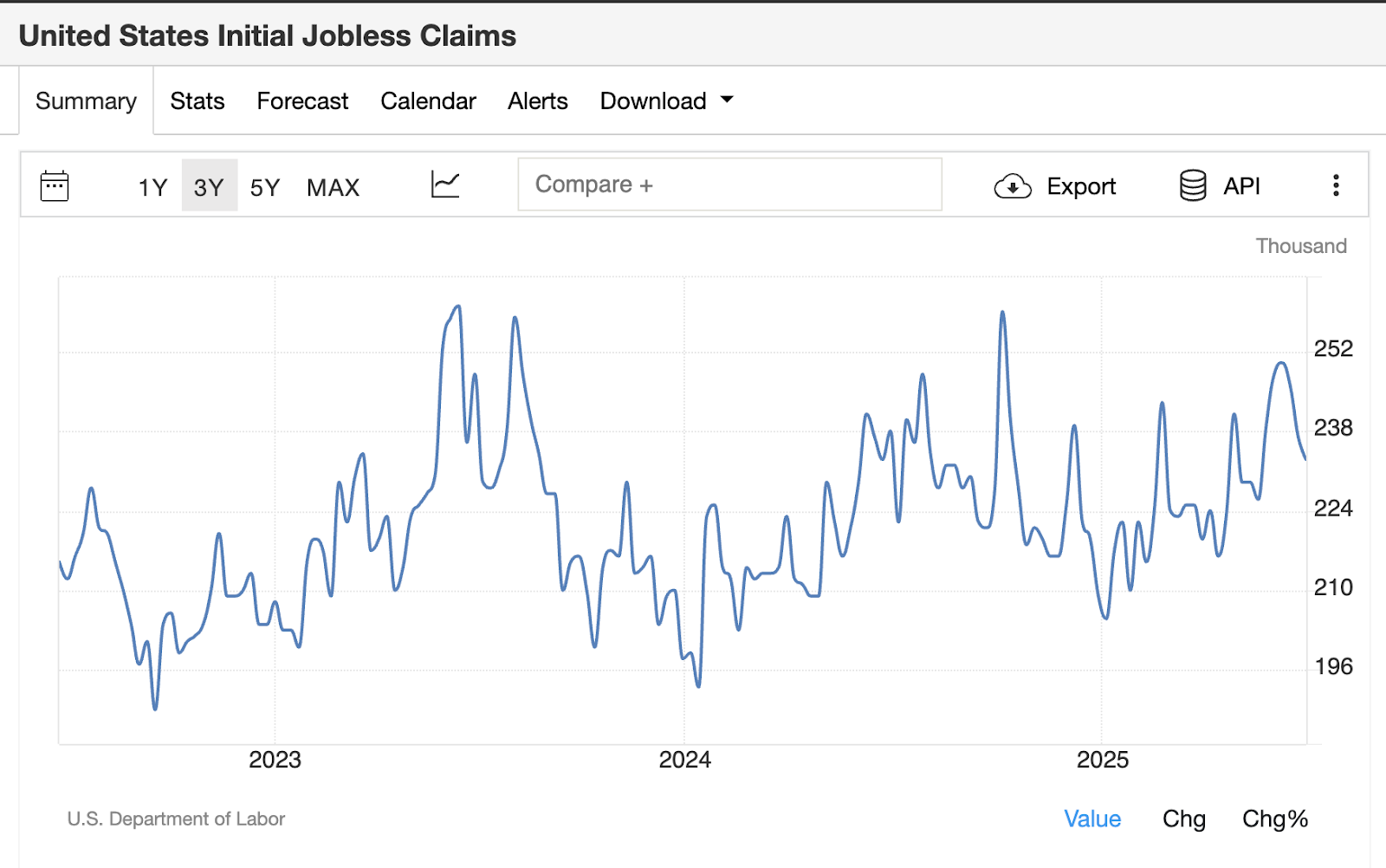

Every week in the midst of a labor market, unemployment claims are grinding more which punishes job seekers.

What is interesting that the economy is not enough to trigger any meaningful pruning cycle. And so, we see that early unemployed claims revolve targetlessly:

Keeping all this together, we have a labor market that has some valid issues – but is not bad enough to trigger any kind of meaningful policy response.

It is rapidly likely that the Fed will continue to sit on his hands and will not take any meaningful step in any direction.

Get news in your inbox. Explore blockwork newsletters: