This is a segment from the forward guidance newsletter. To read full versions, subscribe.

Today, with a hurry to economic figures, it is clear that the American economy is in a very good position, sometimes removing unnatural stop-start tariff saga.

Let’s see the data again and what all this tells us.

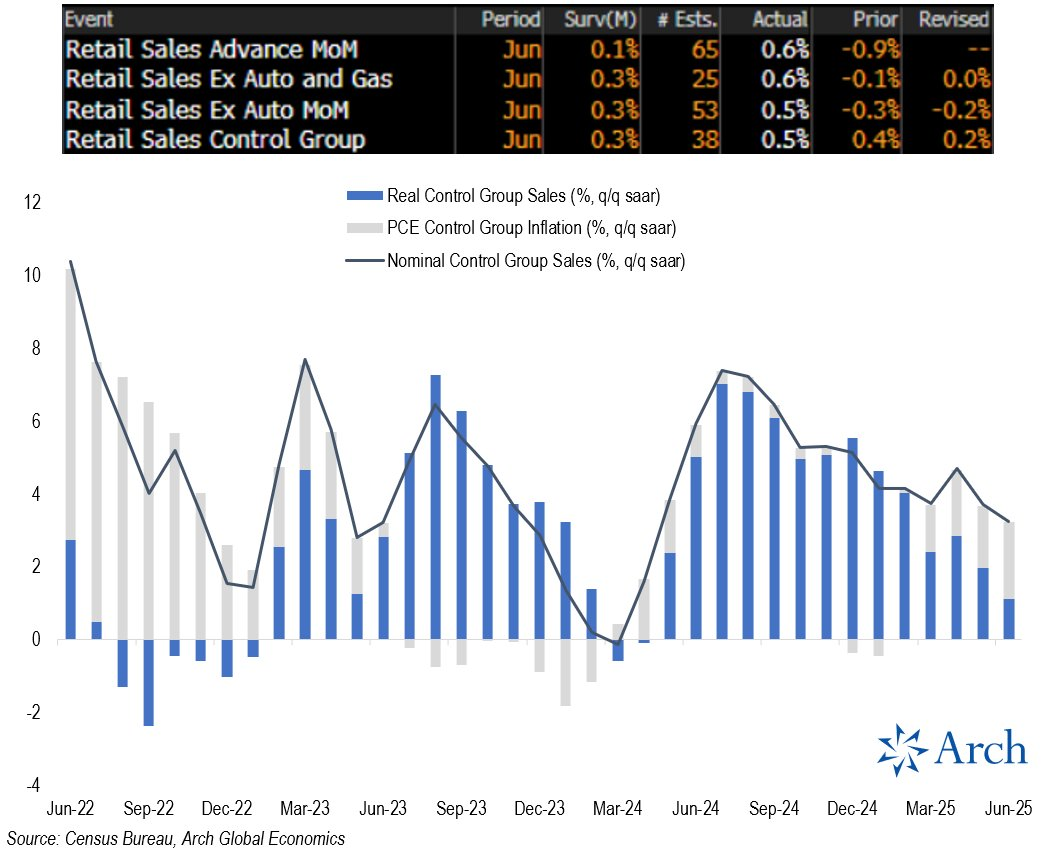

Retail sale

Retail sales came today swinging the gate, defeating the most expectations:

- Retail sale month in a month: real: 0.6%; Expected: 0.1%

- Retail Sales Control Group Mom: Real: 0.5%, Expected: 0.3%

- Retail sales (former auto) mother: real: 0.5%, expected: 0.3%

It is important to remember that retail sales are a nominal metric and therefore includes inflation. In an era of frequent targeted inflation, it becomes rapidly relevant.

Despite the nominal good news, you can see how the purchasing power of consumers is really decreasing. For example, this chart of economist Parker Ross:

This vignet shows why significant recession is difficult to trigger high inflation rule.

A recession can be on a “real” basis – while nominal GDP continues high churning – which lacks net effects purchasing power, as unlike the spending in the economy and nominal reduction in income.

Fed fed survey

Separating hard data, we received an update in the Phili Fed survey, which has been exceptionally accurate in recent years.

This soft data liberation day reflects the clear signals of rebounding of an economy from uncertainty and to adopt where tariffs stand today.

Across the board, each metric continued more:

- Phili Fed Capex Index: Actual 17.10, Previous: 14.50

- Phili Fed Employment: Real: 10.3, Previous: -9.8

- Phili gave new orders: Real: 18.4, Previous: 2.3

- Payment of Phili Fed Prices: Real: 58.80, Previous: 41.40

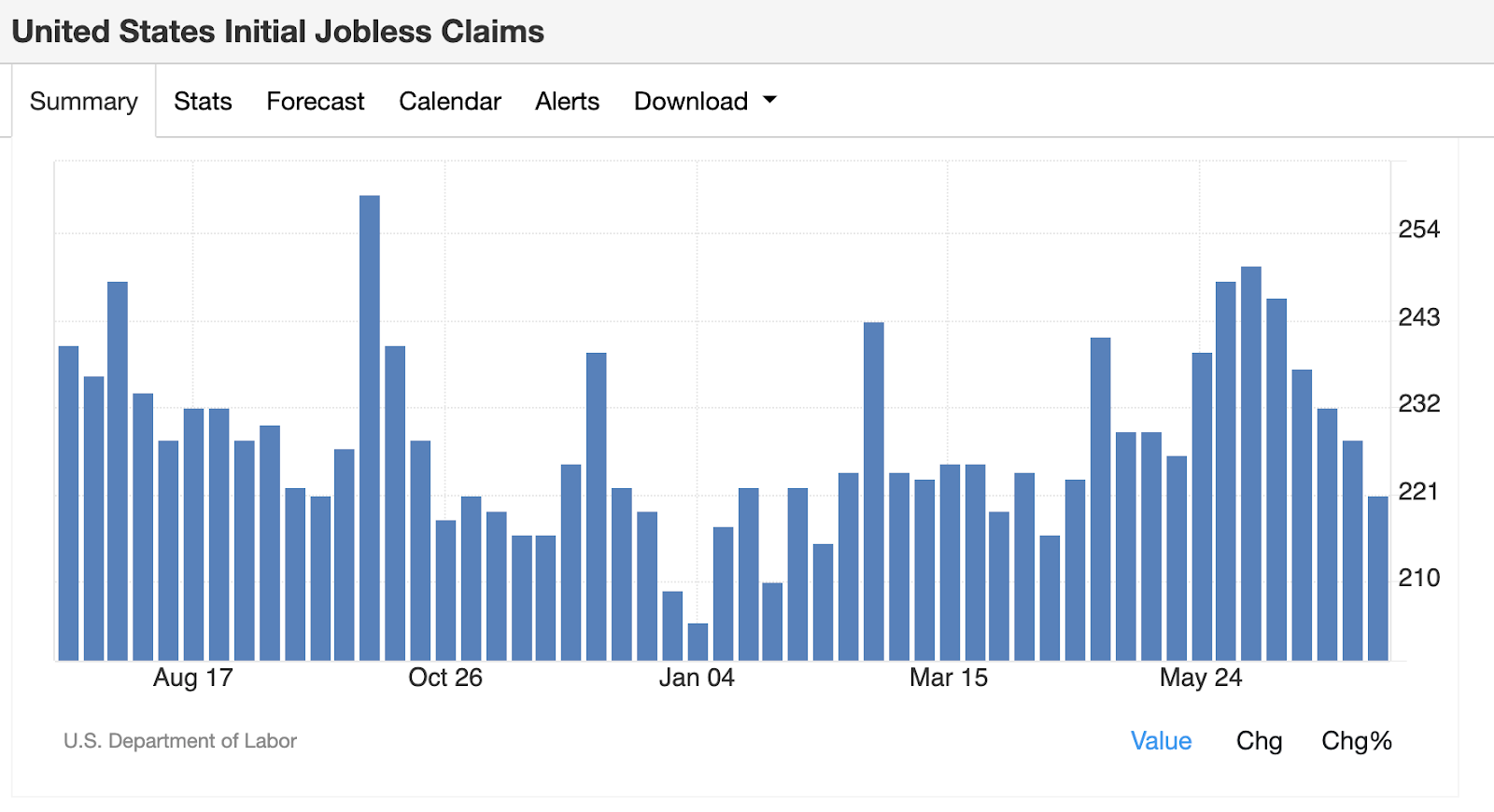

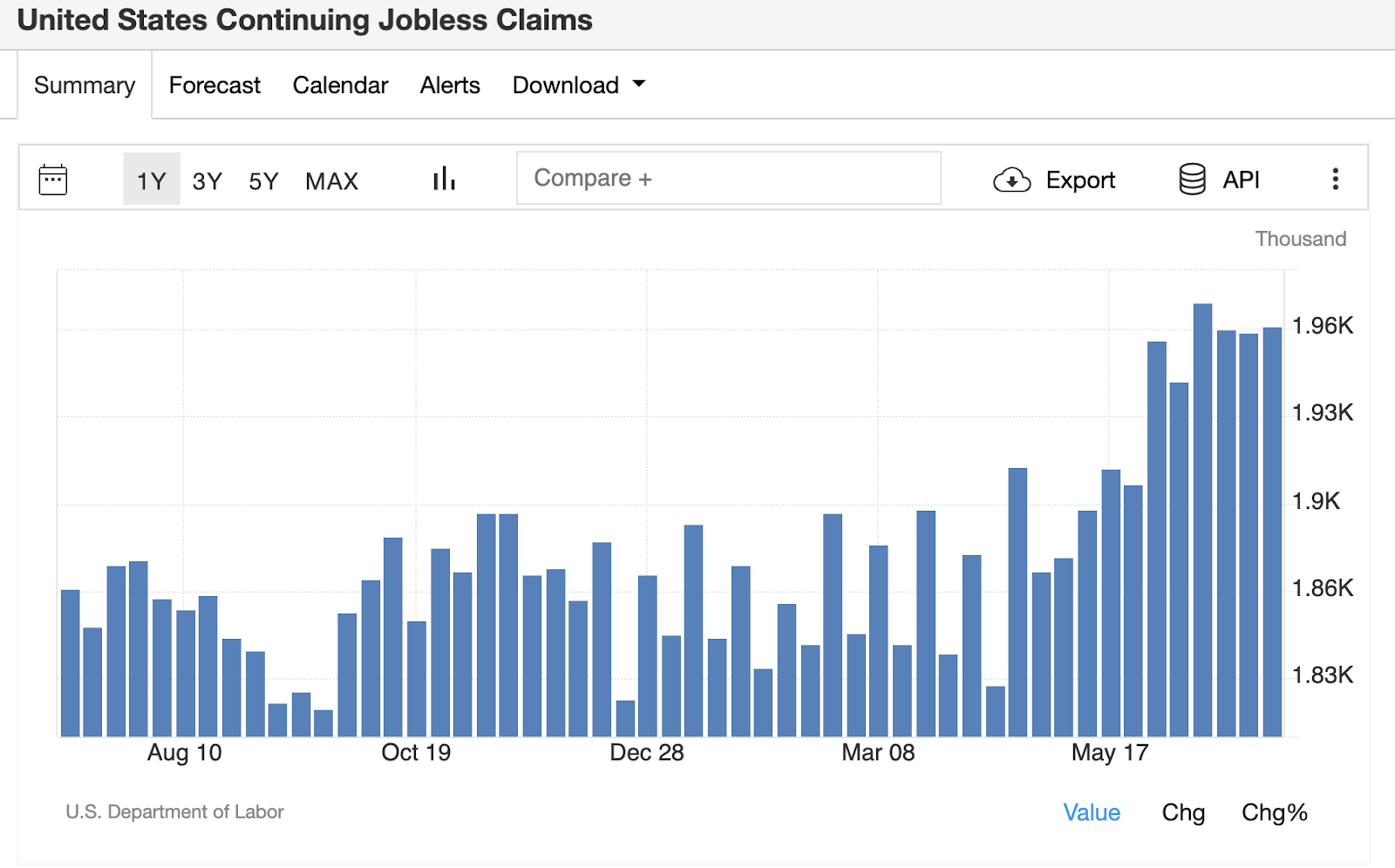

Unemployment allowance

We see the verification of a surprisingly strong economy in data on weekly unemployed claims.

Initial claims surprised the negative side and continued their decline:

Continuing claims also surprised the negative side, showing the sign that recently the bounce has stopped:

It is important to understand the status of the opposite labor market between early and continuous claims. The economy is sufficient solid to avoid triggering a meaningful pruning cycle, but is weak enough so that people who become unemployed are finding difficult times to find a new job and thus remain at constant claims for a long time.

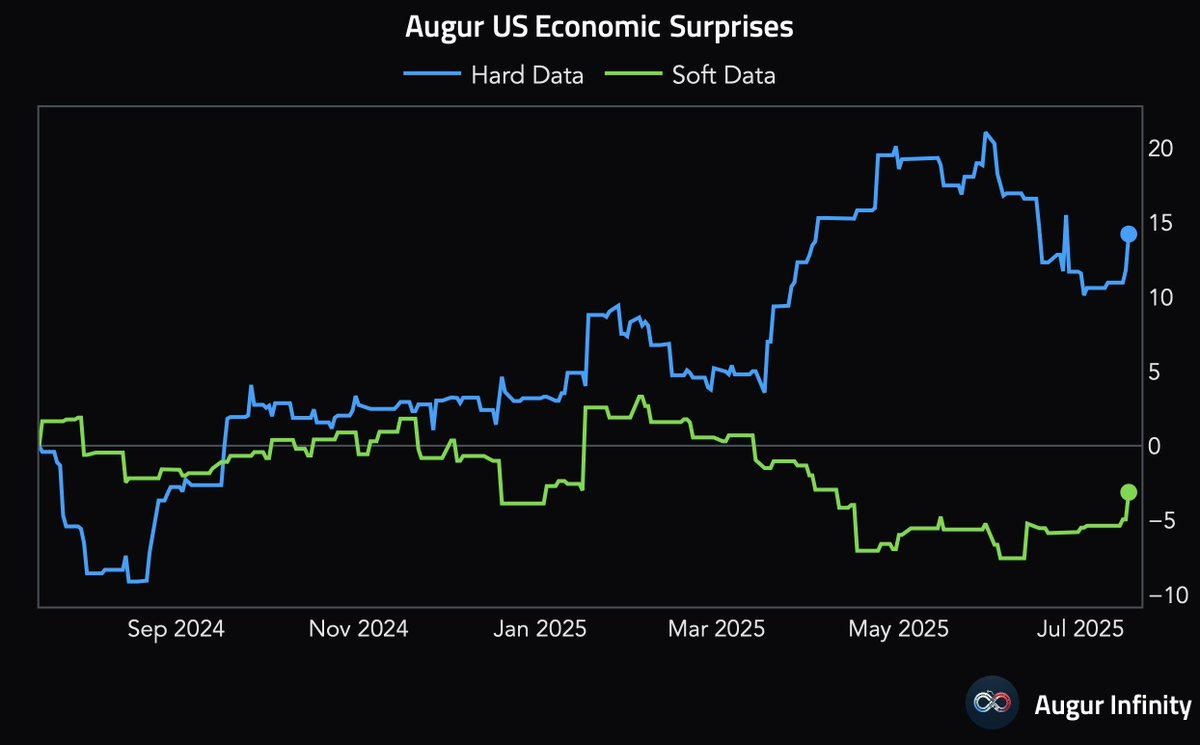

Keeping all this together, it is clear that soft and rigid data are rebound and improvement.

Get news in your inbox. Explore blockwork newsletters: